Bad credit score Impact on Loan & Loan Interest

A person’s creditworthiness is represented numerically by their credit score, which normally ranges from 300 to 850. Your ability to obtain loans and the terms of those loans can be greatly impacted by a poor credit score, which is typically defined as being below 620. This is how your loan facility may be impacted by a low credit score:

The Challenge of Loan Approvals in bad credit score

- Higher Interest Rate ?

The probability of a loan being denied is the most direct effect of a low credit score. A poor credit score is seen by lenders as a sign of increased risk, which makes them reluctant to offer credit.

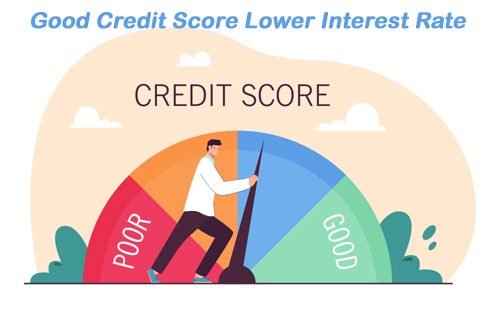

- Higher Interest Rate ?

You will probably pay higher interest rates if you are able to obtain a loan despite having a low credit score. Lenders raise the interest rate on loans to offset the alleged increased risk.

- Higher Down Payment Amounts

Bad credit frequently means higher necessary down payments for secured loans, such as mortgages and vehicle loans. This lessens the risk for the lender.

- Limited Loan Options :

Good credit customers can apply for prime loans from a variety of lenders. Your selections may be restricted to subprime lenders or other loan products if your score is poor, and these products frequently have worse terms.

- Shorter Loan Terms

Lenders may offer shorter repayment periods for borrowers with poor credit, resulting in higher monthly payments but potentially less interest paid over time.

- Additional Fees

Bad credit loans often come with extra fees, such as origination fees or prepayment penalties, further increasing the overall cost of borrowing.

- Stricter Loan Conditions

Lenders might impose stricter conditions, such as requiring a co-signer or collateral, even for loans that typically don’t need them.

- Impact on Credit Limits

If approved for a credit card or line of credit, you’re likely to receive a lower credit limit, restricting your borrowing capacity.

- Employment and Housing Challenges

Some employers and landlords check credit scores. A bad score could potentially affect job prospects or rental applications, indirectly impacting your financial situation.

- Higher Insurance Premiums

In some states, insurance companies use credit scores to determine premiums. A low score could lead to higher costs for auto, home, or other types of insurance.

Conclusion

A bad credit score can have far-reaching consequences on your financial life, particularly when it comes to borrowing money. It’s crucial to understand your credit score and take steps to improve it if necessary. Regularly checking your credit report, paying bills on time, and managing your debt responsibly are key steps toward building a healthier credit profile and improving your loan options in the future.